Filing Requirements

Business Codes

| Business Code | Description | Reporting Purpose |

|---|---|---|

| 017 | Retail/Wholesale |

Retail or wholesale sales of non-marijuana tangible personal property (e.g., marijuana accessories, jars, grow lights, etc.). Wholesale should also report all marijuana sales under 017. |

| 203 | Retail - Medical | Retail sales of medical marijuana (flower/leaf, edibles, etc.). Purchaser must have a prescription and marijuana medical card. |

| 420 | Retail - Adult Use | Retail sales of adult use marijuana and marijuana products (21+ years) (flower, edibles, etc.). |

| 030 | Use Tax - Medical/Adult Use | Cost/value of items used from inventory whether by a retail or wholesaler(free product giveaways, testing, etc.). |

| 029 | Use Tax - Medical/Adult Use | Items purchased from an out-of-state vendor on which no Arizona TPT is collected. |

| 221* | Medical Marijuana Restaurant | Prepared foods infused with medical marijuana intended to be eaten on the premises even if taken to go. |

| 222* | Adult Use Marijuana Restaurant | Prepared foods infused with adult use marijuana intended to be eaten on the premises even if taken to go. |

* Please consult the city rate tables for those cities who charge an additional restaurant tax on the sale of prepared foods infused with medical or adult use marijuana

TPT Tax Rate Table

See marijuana tax rates in the TPT Tax Rate Table, starting on page 21.

Forms

Form MET-1 is the form used to report the adult use marijuana excise tax. The form has an inventory schedule required by statute and should be completed before computing the marijuana excise tax amount. The marijuana excise tax amount is deductible from the retail tax base for TPT purposes. Accordingly, Form MET-1 should be completed prior to completing the TPT return. While all inventory (adult use and medical) is reported on Form MET-1, only the adult use sold to the final consumer is included in column H and used in the tax computation.

The TPT return is the form used to report and remit state/county and city TPT liabilities on all retail sales including the sale of medical or adult use marijuana and anything else sold by the business.

Form 5000 Exemption Certificate

Form 5000A Resale Exemption Certificate

How to File

After a taxpayer obtains an ADHS license to sell medical and/or adult use marijuana and an ADOR TPT license and a MET registration number, as applicable, has been obtained (see licensing above), the taxpayer must report and remit their tax liability monthly on the TPT return. Additionally, the taxpayer must also report and remit the marijuana excise tax using Form MET-1. Taxpayers with a total annual tax liability, or anticipated liability, of $500 must file electronically (A.R.S. § 42-5014(N)).

The reporting and remitting of transaction privilege and excise taxes must be completed online at www.AZTaxes.gov.

Marijuana Excise Tax Return (MET-1)

Form MET-1 should be completed before the TPT return. Form MET-1 reports the inventory changes of all marijuana and marijuana products of the business (adult use and medical) in a reporting period. It also reports net sales to the final consumer of adult use/recreational marijuana and calculates the marijuana excise tax due in a reporting period.

Reporting Inventory Changes

Inventory (Form MET-1 Section II) is reported by the taxpayer’s TPT location (similar to reporting TPT). The taxpayer will report the inventory movement by type. The three reporting types are marijuana, edibles, and other. "Marijuana" includes all flower or leaf products. "Edibles" include such items as brownies, gummies, etc. "Other" is reserved for all types which do not fit in marijuana or edibles; for example, THC infused oils. Inventory which contains less than three-tenths percent on a dry-weight basis of THC has no inventory reporting requirements (i.e., “industrial hemp” as defined in A.R.S. § 3-311).

Taxpayers are required to report the inventory in either grams, pounds, or ounces. If reporting in pounds or ounces, products that are sold in grams will need to be converted to pounds or ounces (total grams divided by 453.592). For example, if a taxpayer sells 500 packages of gummies containing 15 grams of THC, then the inventory will be reported as having sold 16.53 pounds.

7,500 (packages x grams) grams divided by 453.592 equals 16.53.

The starting inventory is reported under Column K. If you have previously filed MET-1 returns, then this should be the ending inventory on your last MET-1 return (Column R). The taxpayer will then report all inventory added to this location. This could be inventory received from the manufacturer or inventory transferred to this reporting location from another one of the business’ locations. The inventory going out is divided into five reported categories:

- Returns to manufacturer/processor (product returned, recalls, etc.);

- Transfers to other retail locations (this includes sale for resale documented with a Form 5000A or intercompany location transfers documented internally);

- Products removed from inventory (testing, samples to customers/employees, etc.);

- Quantity sold to medical cardholders

- Quantity sold for adult use/recreational.

Note: amounts listed as giveaways, taken out of inventory, etc., are subject to use tax and should be reported on the taxpayer’s TPT return.

Excise Tax - Reporting Net Sales of Adult/Recreational Marijuana and Calculating Excise Tax Due

Taxpayers should then report the net sale to the final customer in column (H). This amount should not include any tax collected. Only the sales amount to the final customer, by type. This is tallied and brought forward to the excise tax computation on page 1, section III. This amount is multiplied by 16% for the excise tax due.

Please note, line 4 is for ‘excess tax’ and should not be misread as the adult use marijuana excise tax. Excess tax any excise tax collected over 16% is considered additional/excess (not to be confused with TPT collected) and should be reported on line 4 and remitted to the Arizona Department of Revenue.

Once Form MET-1 is completed the taxpayer should complete the TPT form. Note, your net tax due on line 5 will be included in your TPT gross receipts. Although reported, it is not taxable for TPT purposes, and should be deducted using deduction code 807.

TPT - Reporting Sales of Medical, Adult/Recreational Marijuana, and Wholesaler Manufacturer

Medical Marijuana: To report sales for medical marijuana, report gross receipts (see definition) using business code 203 on the TPT return. If any deductions are applicable, they should be deducted on this form. TPT collected or factored is deducted using deduction code 551. See A.R.S. § 42-5061 for a full list of retail deductions and the corresponding deduction codes.

Adult/Recreational Marijuana: To report sales for adult use marijuana, report gross receipts using business code 420. If any deductions are applicable, they should be deducted on this form as mentioned above. Form MET-1 provides the excise tax liability, which was previously reported and remitted. Deduct this amount from the TPT return using deduction code 807 as excise tax collected. TPT collected or factored is deducted using deduction code 551.

To report sales of other tangible personal property, like marijuana accessories, report gross receipts using business code 017 on the TPT return. If any deductions are applicable, they should be deducted on this form (Note: exempt sales should be documented with an exemption certificate.) TPT collected or factored is deducted using deduction code 551.

The cost of the marijuana that was destroyed for testing or given away as samples, etc., is reported under business code 030 on the TPT form. See example below.

Wholesaler/Manufacturer: Wholesalers, manufacturers or processors of medical or adult use marijuana are required to have a TPT license. The TPT license is used to complete the Form 5000 to allow the wholesaler to purchase items that will be used in the manufacture or resale of goods tax exempt. This does not include the purchase of supplies or tools which do not qualify as exempt machinery and equipment or which are consumed by the business (i.e., items used continuously by the business and not to be manufactured, processed or fabricated for sale).

The gross income derived from the business must be reported and all sales derived from sale-for-resale may be deducted. Sales directly to the final consumer are taxable, unless otherwise deductible.

Use - Reporting of Medical, and Adult/Recreational Marijuana, and Wholesaler Manufacturer

Use tax must be paid on products removed from inventory during the Tax Period. This includes: (1) products or materials sent for testing and destroyed during the process; (2) products that were distributed free of charge to staff, customers or anyone else for any purpose; and (3) products unsuitable for sale to final consumers. Please note: accurate records of these transactions are REQUIRED.

Filing Example

Taxpayer, located in Phoenix, sells both adult use and medical marijuana. Starting inventory for the tax period is:

- 15,000 lbs of marijuana.

- 100 packages of brownies (25 grams THC/package).

- 1,000 packages of gummies (15 grams THC/package).

Inventory activity for the tax period:

- Received shipment of 80,000 lbs of marijuana.

- Gave away 70 samples of 5 grams of marijuana (cost of $600).

- 1 pound of marijuana was sent for testing and was ultimately destroyed (cost of $450).

- Received shipment of 200 packages of brownies.

- Received shipment of 500 jars of budders (22 grams THC/jar).

- Returned 50 packages of brownies to the manufacturer.

Inventory sales include:

- Sold 20,000 lbs for medical use and 40,000 lbs of marijuana for adult use. Adult use net sales of $24,000,000.

- Sold 200 packages of gummies for medical use and 300 packages of gummies for adult use. Adult use net sales of $9,600.

- Sold 50 packages of brownies for adult use and 75 packages of brownies for medical use. Adult use net sales of $250.

- Sold 135 jars of budders for medical use and 275 jars of budders for adult use. Adult use net sales of $11,000.

Taxpayer now prepares the Form MET-1 inventory and net sales starting with the inventory schedule:

Inventory Schedule

Note: The Excise Tax Due is reported on the TPT return as a deduction from gross receipts if included in the gross receipts amount.

The additional information in total sales for medical marijuana include the following:

Additional Sales

- Marijuana sales for medical use of $12,000,000.

- Gummy sales for medical use of $6,400.

- Brownie sales for medical use of $375.

- Budder sales for medical use of $5,400.

- Paraphernalia (hats, vape pens, etc.) of $4,500.

Taxpayer completes the State/County Transaction Detail, the City Transaction Detail and the Schedule A Deductions - State/County and the Schedule A Deductions - City.

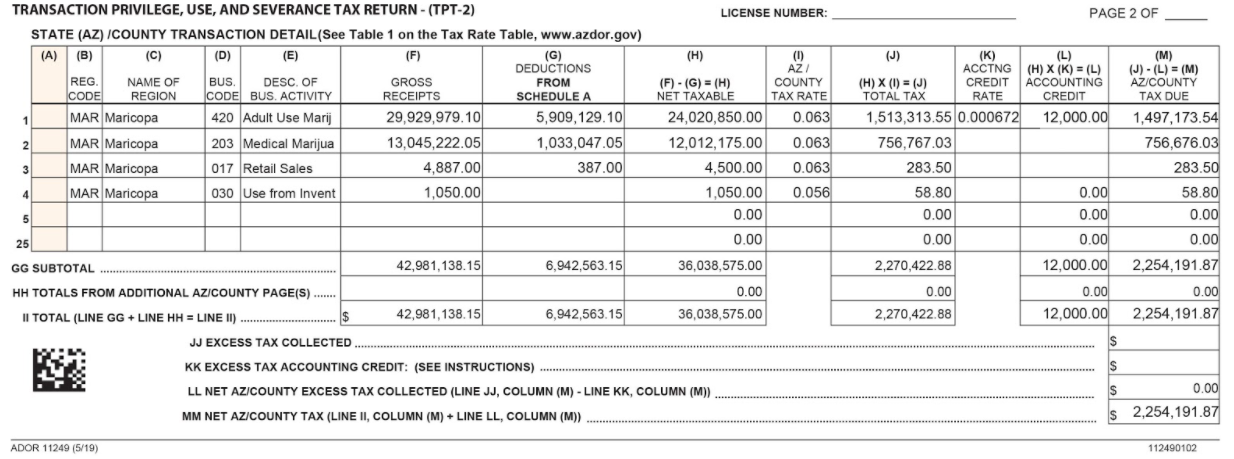

State/County Transaction Detail

*Please note:

- Electronic TPT filers are able to claim an accounting credit of 1.2 percent of the tax due, up to a maximum credit of $12,000, during a calendar year.

- Paper TPT filers are able to claim an accounting credit of 1 percent and a total calendar year credit of $10,000.

Taxpayers who do not file all their TPT returns electronically for the calendar year do not qualify for the additional $2,000 accounting credit.

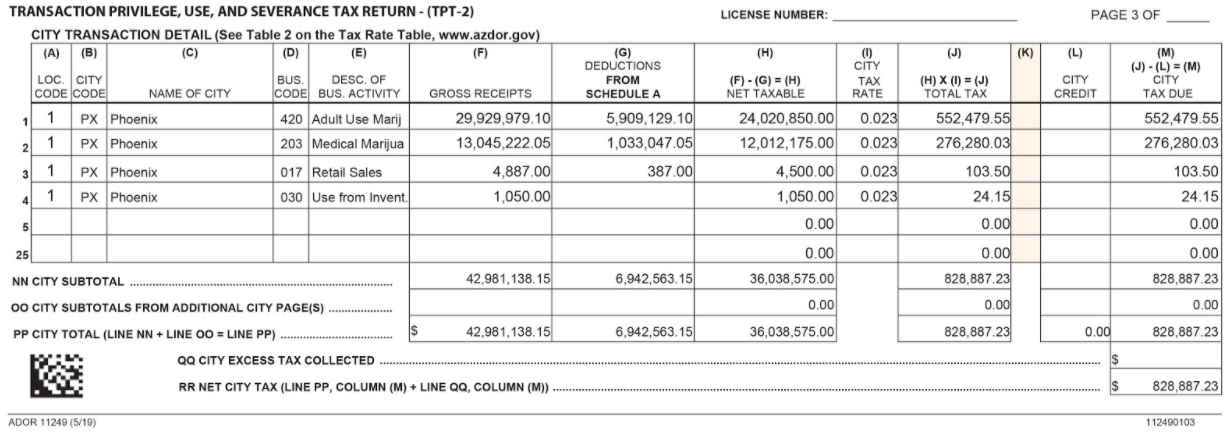

City Transaction Detail

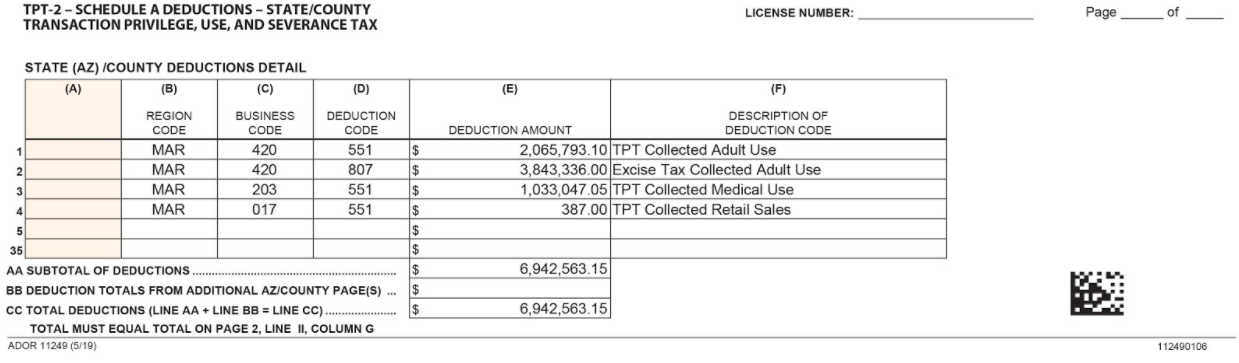

Schedule A Deductions - State County

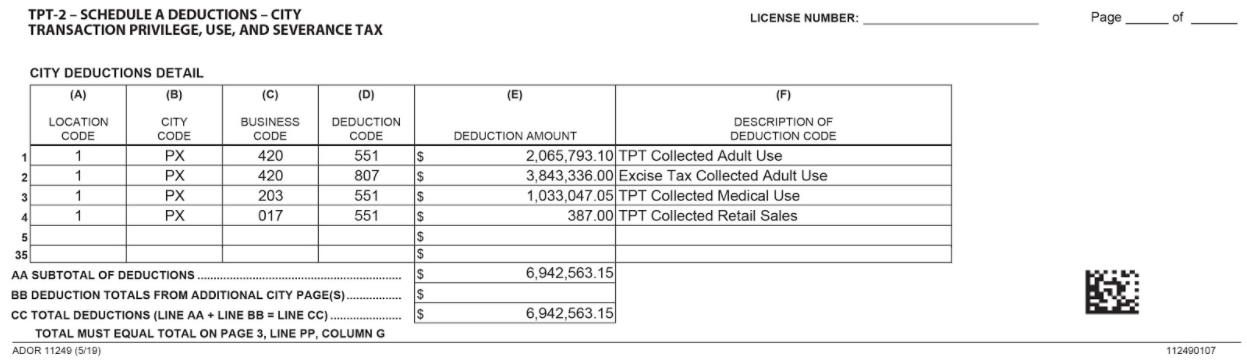

Schedule A Deductions - City

When to File

The Form MET-1 and TPT returns are due on the 20th day of the month following the taxable activity month. Form MET-1 is delinquent if the Department does not receive the form by the 10th day after the due date (Note: this is only the MET-1 return). The TPT return is due on the 20th of the month. For taxpayers that are required to file and pay electronically, the TPT return is delinquent if not received by the Department on or before the last business day of the month.

Payment Waiver Application

All taxes, except individual income, are required to be remitted through the Electronic Funds Transfer (EFT) system if a taxpayer’s liability is greater than or equal to $500 in tax year 2021 and after. See A.R.S. 42-5014(N). However, any taxpayer subject to these rules, including a marijuana establishment, may apply for an annual waiver from the electronic payment requirement. The waiver application must be received by December 31 of each year. The director may grant the waiver if any of the following apply:

- Taxpayer does not have a computer.

- Taxpayer has no internet access.

- Any other circumstance considered to be worthy by the director exists, including:

- Taxpayer has a sustained record of timely payments, and,

- Taxpayer does not have any delinquent tax accounts with the Department.

Available Resources

The Arizona Department of Revenue (ADOR) offers video tutorials under Taxpayer Education that can help you with your TPT filing and other topics.

Power of Attorney: If you need to file a power of attorney form to speak about an marijuana excise tax account, this video can help with completing the form properly.